GSIS MPL Flex: Savior or Trap? An Honest Review for Teachers

EvEvan

January 11, 2026

GSIS MPL Flex: Savior or Trap? An Honest Review

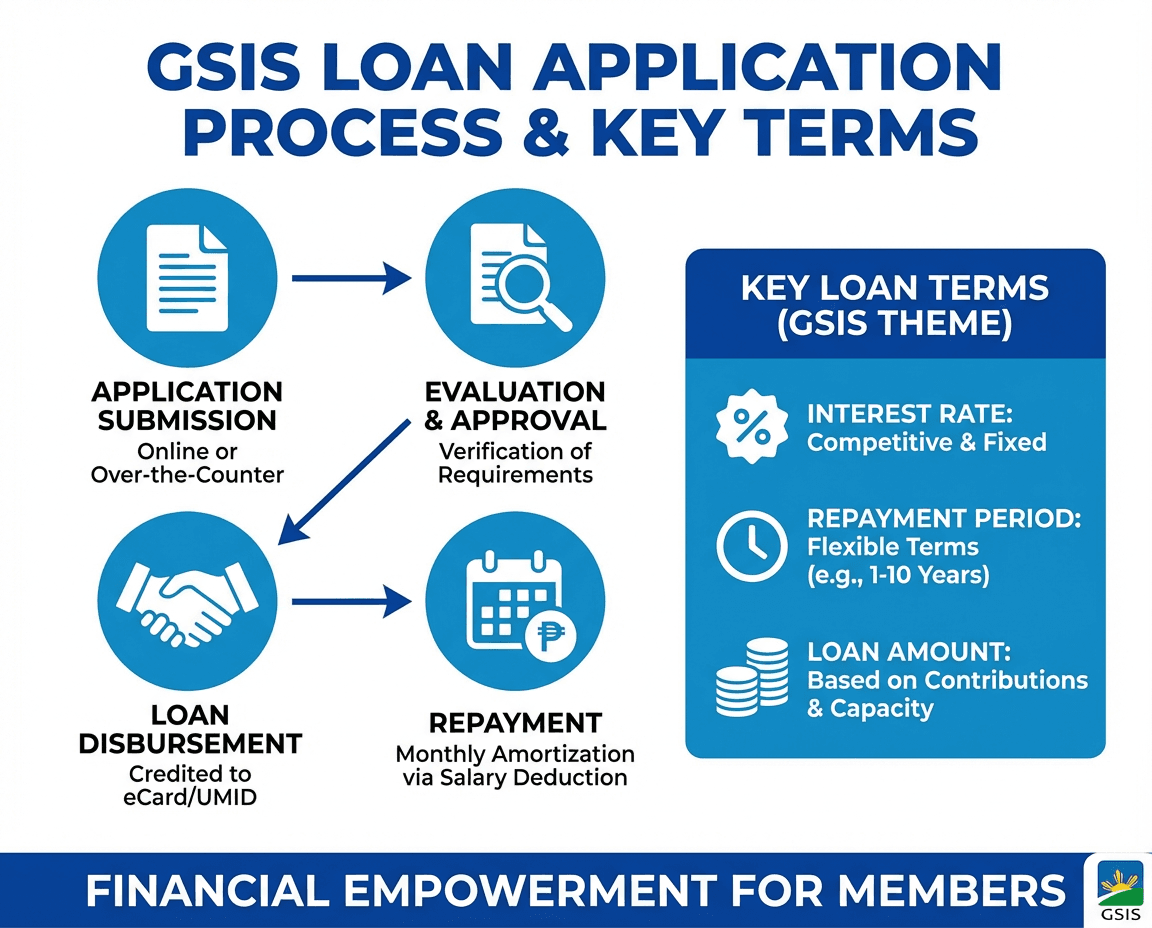

"Loan" is practically a vocabulary word in the DepEd dictionary. Whether it's for house repairs, tuition, or consolidating other debts, we often turn to GSIS.

The latest offering is the MPL Flex (Multi-Purpose Loan Flex). Is it good for you? Let's break it down based on the latest 2025 guidelines.

The Good News

- Longer Terms: You can stretch payment up to 15 years. This lowers your monthly amortization significantly, which is great for keeping your Net Take Home Pay (NTHP) above the mandatory threshold.

- Consolidation: It cleans up your old salary loans and emergency loans into one account, simplifying your payslip.

- Flexibility: As the name implies, you have more options on how to structure the payment compared to the old Conso-Loan.

The Not-So-Good News

- Processing Time: While GSIS claims faster processing via the GSIS Touch App, many teachers in the forums are complaining about delays, especially with the "Form 1.0" or agency verification issues. If the AAO (Agency Authorized Officer) is slow, your loan is slow.

- Interest Accumulation: Longer term = More interest paid over time. Paying for a loan for 15 years means you are paying significantly more than the principal. It is a long commitment.

The Verdict?

If you are drowning in small, high-interest loans from private lenders (the dreaded "London" loans), the MPL Flex is a lifesaver. It consolidates everything at a lower rate.

But, be careful. Don't max out the 15 years if you don't have to. Future-You will thank Present-You for choosing a shorter term. And please, check your GSIS Touch app regularly to make sure your payments are actually being posted!

Ev

Evan

genki